In the latest federal Budget announcement, the commentary from Phillip Coorey, The Australian’s Political Editor, captures the scene vividly: “Jim Chalmers is like a bloke who successfully dieted for two years but crumbled after someone shoved a bucket of KFC under his nose.”

This humorous yet sharply insightful remark highlights the shifts and challenges in the current budget strategy, reflecting the delicate balancing act faced by the Treasurer in managing the nation’s finances amid the cost-of-living crisis.

As we delve deeper into the details of this budget, let us explore how these financial decisions are set to impact Australian businesses and the broader economy:

Personal Income Tax – Cost of Living – increasing the Medicare levy low–income thresholds

The Government has increased the Medicare levy low-income thresholds for singles, families, and seniors and pensioners from 1 July 2023 to provide cost-of-living relief. The increase to the thresholds ensures that low income individuals continue to be exempt from paying the Medicare levy or pay a reduced levy rate.

The increase to the thresholds accounts for recent annual CPI outcomes and is estimated to decrease receipts by $640 million over the four years to 2026–27.

The threshold for singles has been increased from $24,276 to $26,000. The family threshold has been increased from $40,939 to $43,846. For single seniors and pensioners, the threshold has been increased from $38,365 to $41,089. The family threshold for seniors and pensioners has been increased from $53,406 to $57,198. The family income thresholds will now increase by $4,027 for each dependent child, up from $3,760.

This measure has already been provisioned for by the Government.

Source: Budget Paper No 2, p 12.

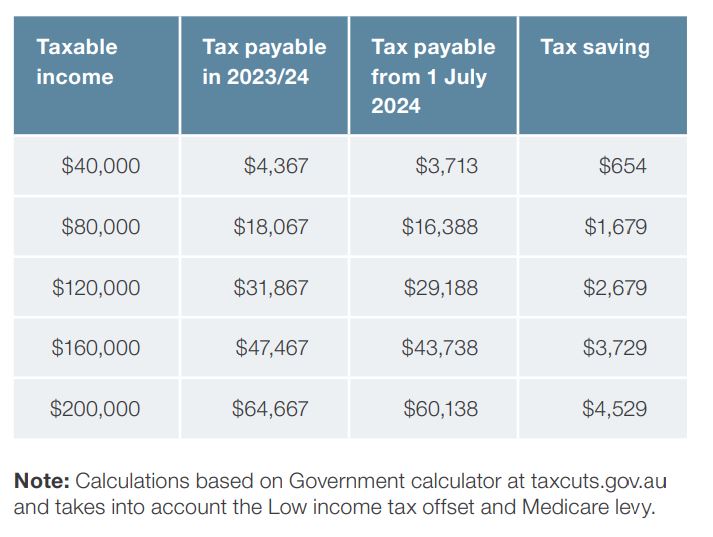

Personal Income Tax – Cost of Living Tax Cuts

The Government has legislated permanent tax cuts for all 13.6 million Australian taxpayers from 1 July 2024.

The tax cuts provide cost-of-living relief, return bracket creep, support women and boost labour supply.

The Government’s tax changes provide bigger tax cuts for more taxpayers, delivering meaningful cost-of-living relief to middle Australia without adding to inflationary pressures.

Under the Government’s tax cuts, from 2024–25:

• the 19 per cent tax rate will be reduced to 16 per cent

• the 32.5 per cent tax rate will be reduced to 30 per cent

• the income threshold above which the 37 per cent tax rate applies will be increased from $120,000 to $135,000

• the income threshold above which the 45 per cent tax rate applies will be increased from $180,000 to $190,000.

This measure is estimated to decrease receipts by $1.3 billion over the 5 years from 2023–24.

Source: Budget Paper No 2, p 12-13.

Small Business Support – $20,000 instant asset write-off

The Government will continue to improve cash flow and reduce compliance costs for small businesses by extending the $20,000 instant asset write-off by 12 months until 30 June 2025.

Small businesses, with an aggregated annual turnover of less than $10 million, will continue to be able to immediately deduct the full cost of eligible assets costing less than $20,000 that are first used or installed ready for use by 30 June 2025. The asset threshold applies on a per asset basis so small businesses can instantly write off multiple assets.

Assets valued at $20,000 or more (which cannot be immediately deducted) can continue to be placed into the small business simplified depreciation pool and depreciated at 15 per cent in the first income year and 30 per cent each income year thereafter.

The provisions that prevent small businesses from re-entering the simplified depreciation regime for five years if they opt-out will continue to be suspended until 30 June 2025.

Source: Budget Paper No 2, p 14-15.

Strengthening Tax Compliance – extending the Personal Income Tax Compliance Program

The Government will extend the ATO Personal Income Tax Compliance Program for one year from 1 July 2027.

This extension will enable the ATO to continue to deliver a combination of proactive, preventative and corrective activities in key areas of non-compliance, including overclaiming of deductions, incorrect reporting of income and inappropriate tax agent influence. This will enable the ATO to continue its focus on emerging risks to the tax system, such as deductions relating to short-term rental properties.

Source: Budget Paper No 2, p15.

Strengthening Tax Compliance – Australian Taxation Office Counter Fraud Strategy

The Government will provide $187.0 million over four years from 1 July 2024 to the ATO to strengthen its ability to detect, prevent and mitigate fraud against the tax and superannuation systems.

Funding includes:

• $78.7 million for upgrades to information and communications technologies to enable the ATO to identify and block suspicious activity in real time

• $83.5 million for a new compliance taskforce to recover lost revenue and intervene when attempts to obtain fraudulent refunds are made

• $24.8 million to improve the ATO’s management and governance of its counter-fraud activities, including improving how the ATO assists individuals harmed by fraud.

The Government will also provide $0.4 million over four years from 1 July 2024 to the Department of Finance to undertake a Gateway Review process over the life of the proposal to ensure independent assurance, oversight and delivery of the measure.

Further, the Government will strengthen the ATO’s ability to combat fraud by extending the time the ATO has to notify a taxpayer if it intends to retain a business activity statement (BAS) refund for further investigation. The ATO’s mandatory notification period for BAS refund retention will be increased from 14 days to 30 days to align with time limits for non-BAS refunds.

The extended period will strengthen the ATO’s ability to combat fraud during peak fraud events like the one that triggered Operation Protego. Legitimate refunds will be largely unaffected. Any legitimate refunds retained for over 14 days would result in the ATO paying interest to the taxpayer (as is currently the case). The ATO will publish BAS processing times online.

This will have effect from the start of the first financial year after Royal Assent of the enabling legislation.

Source: Budget Paper No 2, p 15-16.

Strengthening Tax Compliance – extending the Shadow Economy Compliance Program

The Government will extend the ATO Shadow Economy Compliance Program for two years from 1 July 2026.

This extension of the Shadow Economy Compliance Program will enable the ATO to continue to reduce shadow economy activity, thereby protecting revenue and preventing non-compliant businesses from undercutting competition.

Source: Budget Paper No 2, p16.

Strengthening Tax Compliance – extending the Tax Avoidance Taskforce

The Government will extend the ATO Tax Avoidance Taskforce for two years from 1 July 2026.

Extending the Taskforce ensures the ATO continues to be well-resourced to pursue key tax avoidance risks, with a focus on multinationals, large public and private businesses, and high-wealth individuals.

Source: Budget Paper No 2, p17.

Strengthening the foreign resident capital gains tax regime

The Government will strengthen the foreign resident capital gains tax (CGT) regime to ensure foreign residents pay their fair share of tax in Australia and to provide greater certainty about the operation of the rules. The amendments will apply to CGT events commencing on or after 1 July 2025 to:

• clarify and broaden the types of assets that foreign residents are subject to CGT on

• amend the point-in-time principal asset test to a 365-day testing period

• require foreign residents disposing of shares and other membership interests exceeding $20 million in value to notify the ATO, prior to the transaction being executed.

This measure will ensure that Australia can tax foreign residents on direct and indirect sales of assets with a close economic connection to Australian land, more in line with the tax treatment that already applies to Australian residents. The new ATO notification process will improve oversight and compliance with the foreign resident CGT withholding rules, where a vendor self-assesses their sale is not taxable real property.

These reforms will also improve certainty for foreign investors by aligning Australia’s tax law for foreign resident capital gains more closely with OECD standards and international best practice.

The Government will consult on the implementation details of the measure.

Source: Budget Paper No 2, p 17-18.

Australian Universities Accord – tertiary education system reforms

The Government will provide $1.1 billion over five years from 2023–24 (and an additional $2.7 billion from 2028–29 to 2034–35) for the first stage of reforms to Australia’s tertiary education system in response to the Australian Universities Accord Final Report. These reforms will boost equity and access to higher education, progress tertiary harmonisation and will support a target of 80 per cent of the working age population holding a tertiary qualification by 2050.

Source: Budget Paper No 2, p 62.

Future Made in Australia – Attracting Investment in Key Industries

The Government will provide $68.0 million over four years from 2024–25 (and $3.1 million per year ongoing) to attract investment in key industries to support a Future Made in Australia.

Source: Budget Paper No 2, p 65.

Future Made in Australia – Investing in Innovation, Science and Digital Capabilities

The Government will provide $1.7 billion funding over ten years from 2024–25 for investments in innovation, science and digital capabilities to support a Future Made in Australia.

Source: Budget Paper No 2, p 66.

Future Made in Australia – Making Australia a Renewable Energy Superpower

The Government will provide an estimated $19.7 billion over ten years from 2024–25 to accelerate investment in Future Made in Australia priority industries, including renewable hydrogen, green metals, low carbon liquid fuels, refining and processing of critical minerals and manufacturing of clean energy technologies including in solar and battery supply chains. Funding will catalyse clean energy supply chains and support Australia to become a renewable energy superpower.

Source: Budget Paper No 2, p 67.

Future Made in Australia – Promoting Sustainable Finance Markets

The Government will provide $17.3 million over four years from 2024–25 (and $3.1 million per year ongoing) to promote the development of sustainable finance markets in Australia.

Source: Budget Paper No 2, p 70.

Future Made in Australia – Strengthening Approvals Processes

The Government will provide $182.7 million over eight years from 2023–24 (and $4.5 million ongoing from 2031–32) to strengthen approval processes to support the delivery of the Government’s Future Made in Australia agenda, including Australia’s transition to a net zero economy.

Source: Budget Paper No 2, p 71.

Future Made in Australia – Workforce and Trade Partnerships for Renewable Energy Superpower Industries

The Government will provide $218.4 million over eight years from 2023–24 (and $1.3 million per year ongoing) to support a Future Made in Australia through the development of a skilled and diverse workforce and trade partnerships.

Source: Budget Paper No 2, p 72.

Housing Support

The Government will provide additional funding to build more homes for Australians sooner, invest in more housing enabling infrastructure, train more construction workers and support social and affordable housing and homelessness services.

Funding includes:

• subject to states and territories signing the new National Agreement on Social Housing and Homelessness:

– $423.1 million over five years from 2024–25 in additional funding to support the provision of social housing and homelessness services by states and territories under a new National Agreement on Social Housing and Homelessness. The additional funding will increase annual funding under the new agreement to $1.8 billion per year from 2024–25, with over $9.28 billion provided to states and territories over the life of the agreement

– $1.0 billion in 2023–24 for states and territories to support enabling infrastructure for new housing through a new Housing Support Program – Priority Works Stream

• supporting more community housing providers to access finance through the Affordable Housing Bond Aggregator by increasing the cap on the Government’s guarantee of Housing Australia’s liabilities by $2.5 billion to $10.0 billion, with an associated increase in the line of credit that supports the Affordable Housing Bond Aggregator of $3.0 billion to $4.0 billion

• $88.8 million over three years from 2024–25 to support 20,000 new fee-free training places, including increased access to pre-apprenticeship programs, in courses relevant to the construction sector and delivered through TAFEs and industry registered training organisations

• $19.7 million over six years from 2024–25 to support housing research, fast-track feasibility studies on the release of Commonwealth land to support social and affordable housing and maintain Treasury’s capability to develop, advise on and implement housing policy and programs

$7.0 million over three years from 2023–24 to provide targeted assistance to residential builders seeking to obtain accreditation under the Work Health and Safety Accreditation Scheme

• $6.2 million over two years from 2024–25 to support building industry peak employer associations to assist residential builders in obtaining accreditation under the Work Health and Safety Accreditation Scheme

• $2.0 million over three years from 2024–25 to build the financial capability of community housing providers and Aboriginal and Torres Strait Islander community controlled housing organisations

• $1.8 million over two years from 2024–25 for the Department of Employment and Workplace Relations to deliver streamlined skills assessments for migrants from comparable countries who wish to work in Australia’s housing construction industry

• support to increase available rental housing by allowing foreign investors to purchase established Build to Rent properties with a lower foreign investment fee, conditional on the property continuing to be operated as a build to rent development.

In addition, the Government will:

• target the $1.0 billion for social housing under the National Housing Infrastructure Facility in the 2023–24 MYEFO towards crisis and transitional accommodation for women and children fleeing domestic violence, and youth, including redistributing the mix of concessional loans and grants to increase the proportion of grants to $700.0 million

• provide $1.9 billion in concessional finance to support community housing providers to deliver social and affordable housing under the Housing Australia Future Fund and the National Housing Accord.

Source: Budget Paper No 2, p 74 – 75.

Child Care Subsidy Reform – further measures for strong and sustainable foundations

The Government will achieve net savings of $410.7 million over four years from 2024–25 through additional activities to strengthen the payment and accuracy of the Child Care Subsidy program.

The Government will invest $30.0 million over two years from 2024–25 in IT and payment services to deliver on its commitment to provide funding towards a wage increase for the Early Childhood Education and Care sector. This will support a response to Fair Work Commission processes as they relate to this sector.

Source: Budget Paper No 2, p 86.

Closing the Gap – Education

The Government will provide $110.0 million over four years from 2024–25 (and $11.0 million per year ongoing) to accelerate action against the National Agreement on Closing the Gap Priority Reforms in the Education portfolio and extend programs supporting education outcomes.

Source: Budget Paper No 2, p 87.

Inclusion Support Program – additional funding

The Government will provide $98.4 million in 2024–25 to help child care services increase their capacity to support inclusion of children with additional needs, through tailored support and funding to services.

Source: Budget Paper No 2, p 88.

School Education Support

The Government will provide $70.3 million over five years from 2023–24 to continue support for initiatives to improve education outcomes for students.

Source: Budget Paper No 2, p 88.

Australian Apprenticeships Incentive System – further support

The Government will provide $265.1 million over four years from 2024–25 to adjust previously scheduled Phase Two Incentive System payments to provide further support for apprentices, trainees and their employers in priority occupations, while the Government undertakes the Strategic Review of the Australian Apprenticeships Incentive System.

Under 2022–23 March Budget arrangements for the Australian Apprenticeships Incentive System, financial support to apprentices, trainees and their employers was scheduled to reduce from 1 July 2024, including for those in priority occupations, through the implementation of Phase Two settings. The measure will increase Phase Two Incentive System payments for apprentices in priority occupations from $3,000 to $5,000 and hiring incentives for priority occupation employers from $4,000 to $5,000 for 12 months from 1 July 2024.

Source: Budget Paper No 2, p 90.

Employment Services Reform

The Government will provide $13.2 million over five years from 2023–24 (and savings of $36.9 million per year ongoing) for improvements to the employment services system and to support future reform.

Funding includes:

• $68.6 million over five years from 2023–24 to increase resourcing for the Digital Services Contact Centre to support people using Workforce Australia Online services

• $32.1 million over four years from 2024–25 for the Real Jobs, Real Wages pilot providing tapered payments to employers to support wages for people at risk of long-term unemployment

• $21.9 million over five years from 2023–24 to provide paid employment placements through social enterprise and employer partnerships for people with high barriers to work

• $13.0 million over five years from 2023–24 (and $0.9 million per year ongoing) to strengthen the complaints mechanism for clients of Workforce Australia and introduce further safeguards in relation to payment suspensions or penalties

$10.9 million over four years from 2024–25 (and $0.8 million per year ongoing) for critical improvements to the Workforce Australia IT system

• $6.4 million over five years from 2023–24 (and net savings of $0.3 million per year ongoing) to better recognise individuals’ circumstances through more appropriate and consistent application of mutual obligation rules for certain recipients of income support payments.

Source: Budget Paper No 2, p 91 – 92.

Further Support for the Vocational Education and Training System

The Government will provide $26.1 million over four years from 2024–25 for the Skills and Training portfolio to contribute to a strong and effective Vocational Education and Training system, continue structural reforms, and maximise returns on previous skills and training investments and commitments.

Source: Budget Paper No 2, p 94.

Promoting TAFE and VET Pathways

The Government will provide $4.4 million in 2024–25 to drive demand for Vocational Education and Training (VET) in support of delivering the workforce required to meet Australia’s future skills needs. This will include delivering strategic communications to increase the appeal of VET for students, parents and teachers, and extending community awareness of Fee-Free TAFE courses in areas of high skills needs which has ensured strong uptake of Fee-Free TAFE places to date.

Source: Budget Paper No 2, p 95.

Health Workforce

The Government will provide $116.2 million over five years from 2023–24 to strengthen and support the health workforce.

Source: Budget Paper No 2, p 111

Improving Aged Care Support

The Government will provide $2.2 billion over five years from 2023–24 to deliver key aged care reforms and to continue to implement recommendations from the Royal Commission into Aged Care Quality and Safety.

Source: Budget Paper No 2, p 112.

Mental Health

The Government will provide $888.1 million over 8 years from 2024–25 (and $139.8 million per year ongoing) to respond to the Better Access evaluation and to strengthen Australia’s mental health and suicide prevention system.

Source: Budget Paper No 2, p 116.

Pharmaceutical Benefits Scheme (PBS) – new and amended listings

The Government will provide $3.4 billion over five years from 2023–24 for new and amended listings on the Pharmaceutical Benefits Scheme (PBS) and the Repatriation Pharmaceutical Benefits Scheme.

Source: Budget Paper No 2, p 119.

Securing Cheaper Medicines

The Government will provide $480.2 million over five years from 2023–24 to reduce patient costs and improve access to medicines.

Source: Budget Paper No 2, p 124.

Strengthening Medicare

The Government will provide $1.2 billion over five years from 2023–24 ($14.8 million per year ongoing) to strengthen Medicare by supporting earlier discharge from hospital for older Australians, improving access to essential services, modernising Australia’s digital health infrastructure and ensuring the integrity and compliance of Medicare.

Source: Budget Paper No 2, p 126.

Strengthening Medicare – Medicare Urgent Care Clinics – additional funding

The Government will provide $227.0 million over three years from 2023–24 to boost the capacity of Medicare Urgent Care Clinics. This will include a further 29 Medicare Urgent Care Clinics across Australia, which will take the total number of Medicare Urgent Care Clinics to 87. The Government is also providing additional support to clinics in regional and rural Australia.

Source: Budget Paper No 2, p 128.

Strengthening Medicare – an effective and clinically appropriate Medicare Benefits Schedule (MBS)

The Government will provide $895.6 million over four years from 2024–25 to ensure the Medicare Benefits Schedule (MBS) remains clinically appropriate and reflects modern medical practices.

Source: Budget Paper No 2, p 129.

Building a Better Future Through Considered Infrastructure Investment

The Government is committed to delivering the priority road and rail infrastructure projects Australia needs via the over $120.0 billion infrastructure investment pipeline. Building on the Independent Strategic Review of the Infrastructure Investment Program, the Government is taking a more integrated, strategic and sustainable approach to infrastructure investment this Budget.

Source: Budget Paper No 2, p 144.

A Higher Rate of JobSeeker Payment for Participants with a Partial Capacity to Work (0-14 hours)

The Government will provide $41.2 million over five years from 2023–24 (and $7.0 million per year ongoing from 2028–29) to extend eligibility for the existing higher rate of JobSeeker payment to single recipients with a partial capacity to work of zero to 14 hours per week from 20 September 2024.

The higher JobSeeker payment rate is currently provided to single recipients with dependent children and those aged 55 and over who have been on payment for nine continuous months or more.

Source: Budget Paper No 2, p 164.

Carer Payment – increased flexibility

The Government will provide $18.6 million over five years from 2023–24 (and $3.1 million per year ongoing) to support Carer Payment recipients through increased flexibility to undertake work, study and volunteering activities.

From 20 March 2025, the existing 25 hour per week participation limit for Carer Payment recipients will be amended to 100 hours over four weeks. The participation limit will no longer capture study, volunteering activities and travel time and will only apply to employment.

Carer Payment recipients exceeding the participation limit or their allowable temporary cessation of care days will have their payments suspended for up to six months, rather than cancelled. Recipients will also be able to use single temporary cessation of care days where they exceed the participation limit, rather than the current seven day minimum.

Source: Budget Paper No 2, p 166.

Commonwealth Government-Funded Paid Parental Leave – enhancement

The Government will provide $1.1 billion over five years from 2023–24 (and $0.6 billion per year ongoing) to strengthen Australia’s government-funded Paid Parental Leave (PPL) scheme and improve women’s retirement outcomes.

Source: Budget Paper No 2, p 166.

Commonwealth Rent Assistance – increase the maximum rates

The Government will provide $1.9 billion over five years from 2023–24 (and $0.5 billion per year ongoing from 2028–29) to increase all Commonwealth Rent Assistance maximum rates by 10 per cent from 20 September 2024 to help address rental affordability challenges for recipients.

Source: Budget Paper No 2, p 167.

Financial Wellbeing and Capability Activity – additional funding

The Government will provide $138.0 million over five years from 2023–24 (and $35.4 million per year ongoing) to boost support for Australians in financial distress or experiencing financial hardship and to build financial resilience, through additional funding to the Financial Wellbeing and Capability Activity. The activity will also be restructured to operate under two streams of support: Financial Capability and Resilience and Financial Crisis Response and Recovery.

Source: Budget Paper No 2, p 169.

Freeze Social Security Deeming Rates

The Government will freeze social security deeming rates at their current levels for a further 12 months until 30 June 2025, to support Age Pensioners and other income support recipients who rely on income from deemed financial investments, as well as their payment, to manage cost of living pressures.

Source: Budget Paper No 2, p 170 – 171.

National Disability Insurance Scheme – getting the NDIS back on track

The Government is committed to improving outcomes for National Disability Insurance Scheme (NDIS) participants and ensuring every dollar of NDIS funding goes to those who need it most. The Government will provide $468.7 million over five years from 2023–24 (and $37.9 million per year ongoing) to support people with disability and get the NDIS back on track.

Source: Budget Paper No 2, p 172.

Services Australia – additional resourcing

The Government will provide $2.8 billion over five years from 2023–24 (and $144.7 million per year ongoing) to improve the way Services Australia delivers services to the Australian community.

Source: Budget Paper No 2, p 175.

The Leaving Violence Program – financial support for victim-survivors of intimate partner violence

The Government will provide $925.2 million over five years from 2023–24 (and $263.3 million per year ongoing) to make permanent the Leaving Violence Program that will provide financial support, safety assessments and referrals to support services for victim-survivors leaving a violent intimate partner relationship.

Source: Budget Paper No 2, p 176.

Energy Bill Relief Fund – extension and expansion

The Government will provide $3.5 billion over three years from 2023–24 to extend and expand the Energy Bill Relief Fund to provide a $300 rebate to all Australian households and a $325 rebate to eligible small businesses on 2024–25 bills to provide cost of living relief.

Source: Budget Paper No 2, p 179 – 180.

Supporting Small Businesses

The Government will provide $41.7 million over four years from 2024–25 to support small businesses.

Funding includes:

• $25.3 million over four years from 2024–25 to support the Payment Times Reporting Regulator to implement reforms recommended by the statutory review of the Payment Times Reporting Act 2020, including increased resourcing for the Regulator and upgrading the Regulator’s ICT infrastructure

• $10.8 million over two years from 2024–25 to extend the Small Business Debt Helpline and the NewAccess for Small Business Owners program to continue to provide financial counselling and mental health support for small business owners

• $3.0 million over two years from 2024–25 to implement the Government’s response to the Review of the Franchising Code of Conduct, including by investigating the feasibility of a licensing model and remaking and updating the Franchising Code of Conduct prior to its expiration in April 2025

• $2.6 million over four years from 2024–25 (and $0.7 million per year ongoing) for the Australian Small Business and Family Enterprise Ombudsman to support unrepresented small businesses to navigate business-to-business disputes through alternative dispute resolution.

Source: Budget Paper No 2, p 182 – 183.