| It’s a wonderful feeling when you have got to a point where your business is so successful that you need to upscale. Whether hiring more people or moving location, upscaling has its unique challenges. What can you do to ensure that you are hitting the ground running while upscaling? Set Realistic And Actionable Goals Businesses should set realistic and actionable small goals which they can work towards, rather than broad goals which provide no direction. Setting broad and unrealistic goals is demotivating and makes any progress made seem insignificant. Every person in the business should be given a target to meet over a reasonable timeline, contributing to achieving a larger goal. Establish Standardised And Automated Processes Small businesses can make the mistake of ‘doing things as they come’ but this means that as the business grows, adjusting to high-scale tasks is difficult. To avoid this, businesses should standardise all processes of work. Any individual placed into a role should be able to follow standardised procedures and yield a product that is of similar quality to the previous one. Investing money into automation tools is worthwhile for this procedure. This can include automating social media management, email, and customer relationships. Both of these will contribute to creating structures that support growth. Identify Competitive Strengths And Weaknesses Recognising the strengths and weaknesses of one’s business is essential. Strengths will allow businesses to hone their unique qualities, giving them a competitive advantage. Weaknesses will reveal which areas require growth so that changes can be made before upscaling takes place. Network Businesses should continue to develop relationships with service providers, sales channel partners, suppliers and customers. Keeping an open mind about partnerships or potential collaborations could open up different avenues of business growth. Anticipate The Adjustment Pace. No matter how prepared you feel, any change in an organisation will require a period of adjustment for the rest of your team. Give them time to recognise the need for change and accept this opportunity’s challenges. More importantly, they need time to understand their roles in the bigger picture of your organisation’s plans to scale and determine how they can make the most of their skill sets and add value to the company. Make sure to consider adjustment protocols and allocate a reasonable period for such adjustments in your scaling plans and process. Outsourcing The Non-Essentials As the business increases in stature, there will be a lot more little and frustrating tasks, meaning that you can’t focus on what’s important. Outsourcing components like payroll or marketing to companies with the professionals to do it effectively means that you can focus on upscaling the business. Upscaling can be a very stressful process, but whether it’s making changes to your business’s technology or outsourcing things in the short term, to upscale a business means focusing on what is best for your business. To get to this point, you’ve made a success of it, so it’s important not to lose your identity in the process. Upscaling your business is taking what’s great about your current operation and building it outwards. If you are looking towards how your business can take itself to the next level, business planning for any eventualities can be of benefit. Consulting with a Leenane Templeton trusted adviser can be of great help when moving forward in your business’s upscaling endeavour. Contact us today. |

Disclaimer: The information contained in this publication is for general information purposes only, professional advice should be obtained before acting on any information contained herein. The receiver of this document accepts that this publication may only be distributed for the purposes previously stipulated and agreed upon at subscription. Neither the publishers nor the distributors can accept any responsibility for loss occasioned to any person as a result of action taken or refrained from in consequence of the contents of this publication. |

Author: Harlan Marriott

-

Looking To Upscale Your Business? Here’s What You Need To Know…

-

What Happens To A Loved One’s Superannuation In The Event Of Dementia?

Superannuation can be confusing at the best of times for the average Australian. However, for those experiencing the effects of mental impairment (such as dementia), or living with those affected by it, access to their superannuation can become a financial issue of great magnitude.

Dementia is not a specific disease, but rather a term that describes symptoms associated with more than 100 different diseases characterised by the impairment of brain function. The most common type of dementia that is often encountered is Alzheimer’s disease.

It occurs more frequently in the elder demographic than in the younger population but is indiscriminate in who it affects. However, with an increasing number of people looking at accessing their superannuation, and a rise in the number of Australians impacted by Alzheimer’s disease or other forms of dementia, it’s best to be prepared with the knowledge of what you must do.

When it comes to your superannuation, if your circumstances mark you as an eligible applicant, you may be able to claim a lump sum from your superannuation fund’s total and permanent disability (TPD) insurance.

You may be under the assumption that to access the benefits from TPD, you need to have suffered an accident, a workplace injury or a critical terminal illness. However, you can claim for TPD and monthly income protection benefits from your super fund if you have any type of long-term illness that affects your ability to do your job (including young-onset Alzheimer’s or dementia).

You should get total and permanent disablement from your life insurance provider for a broad range of early-onset Alzheimer’s disease or dementia-related symptoms, including significant permanent impairment, loss of independence, cognitive decline, and other mental health effects.

Your life insurance provider will consider several factors when deciding whether you’re eligible to make a claim, including:

• Whether your claim can be supported by a doctor or medical specialist.

• Whether you’re receiving any treatment for dementia or Alzheimer’s disease, and the frequency of this treatment.

• Whether your early-onset Alzheimer’s disease can be considered permanent.

• How your capacity to work has been impaired or will be impaired by your symptoms as your disease progresses.

• Whether you may be able to take on an adjusted job role or work in a new career.If you successfully claim TPD insurance for early-onset Alzheimer’s or dementia, you should be given early access to your super. This money will be paid in a lump sum and will cover your day-to-day costs for the rest of your life. The amount of money you receive will depend on your specific circumstances

What About If An SMSF Trustee Is Affected By Dementia/ Alzheimer’s?

In the case of an SMSF, legally, the loss of mental capacity for a trustee of an SMSF means that they can no longer make decisions as a trustee of the fund. The critical period for an SMSF is the time prior to diagnosis when the trustee may be making or not making decisions that would be in the best interest of the members of the fund.

There are four options that the trustees of this SMSF have:

• They can retain the SMSF and appoint additional trustees to the fund who share trustee responsibility as they age (which would typically occur with adult children joining the fund).

• The trustees of the SMSF can appoint an individual to take on trustee responsibility on his behalf under an enduring power of attorney.

• The trustees of the SMSF can close the SMSF and rollover the fund to a public offer fund, with all ongoing administration and compliance of the fund reverting to a third-party trustee.

• The SMSF trustee can convert the fund into a Small APRA Fund (SAF). A SAF offers the flexibility of an SMSF, without trustee responsibilities as an independent trustee is appointed to manage the trustee responsibilities on an individual fund basis and on an agreed fee basis.

It is most important to remember that if you have not appointed someone as your enduring power of attorney and you do lose mental capacity, then it is too late and you will need to apply to the court. It is always important to seek advice about appointing someone as your enduring power of attorney.

-

Business Automation: How Could You Benefit?

With client needs and team capabilities constantly changing within the business world, we recommend you pause and reflect on your own critical business processes to see if you can spot opportunities for improving efficiency and reducing waste.

There’s no better time to do this than at the start of a new financial year.

Get your team together in a room or a Zoom meeting to brainstorm the processes or work that:

– frustrates them,

– has highly repetitive tasks, or is

– time-consuming.

Then, you should examine how you might be able to automate these processes to improve your business’s productivity and output better.

Business automation can occur in order to improve external performance and experience of the business for your clients OR it can be used to improve upon the internal processes of your business.

For example, communicating with your employees is one constant in your business. This is obviously important, but you know it could be improved. You don’t need to have as many meetings as you are now. You should be able to share feedback faster. So how can this be improved?

Automated business processes can be split into four basic types outlined below.

Basic Automation

Basic automation refers to the most straightforward jobs that need to be performed , like creating a centralized place to store a mix of related information. This can be automated through a project management tool that prioritises collaboration and communication to seamlessly pull together a patchwork of data into a single platform.

This tool should automatically organise all of this information to make it understandable and usable.

Process Automation

Process automation involves a dedicated network of software and apps used to document and manage your business processes, such as budgeting or project management.

Integration Automation

Integration automation allows machines and software to monitor and analyze how employees perform tasks and imitate them. You simply define the rules of operation.

An example would be your project management software integrated with your customer support software. A customer complaint comes through, but instead of waiting in an inbox for someone to process it, the integration automatically sends it as a task to the person assigned to handle them.

Artificial Intelligence (AI) Automation

Artificial Intelligence (AI) automation is when you combine AI with your integrated software tools for faster, more intelligent decision-making. The system can now make choices on your behalf with the data it’s presented.

Some general examples in which your business could benefit from automating key processes could include:

* Email Automation – Automating your inbox can assist in automatically processing information from your email quickly and efficiently

*Automated Business Application Integration – With businesses using more and more different applications, a lot of business processes can involve multiple business applications at the same time

*Automated Order Entry – You can use business process automation to automate your database interaction processes without writing a line of code

*Browser Automation – Even if a part of your process involves going to a website and clicking on fields or grabbing information, business process automation can make it faster and more efficient.

Disclaimer:

The information contained in this publication is for general information purposes only, professional advice should be obtained before acting on any information contained herein. The receiver of this document accepts that this publication may only be distributed for the purposes previously stipulated and agreed upon at subscription. Neither the publishers nor the distributors can accept any responsibility for loss occasioned to any person as a result of action taken or refrained from in consequence of the contents of this publication. -

What Do You Need To Do To Make Your Business Compliant With Superannuation Requirements For Its Employees?

It is your responsibility as an employer to set up your business to pay super into your eligible employees’ chosen super funds or their stapled super fund where no choice has been made.

If your employee hasn’t made a choice and doesn’t have a stapled super fund, you can contribute their super to your default super fund.

What you need to do:

- Select your default super fund.

- Offer employees a choice of super fund and keep records that show you’ve done this.

- Request your employee’s stapled super fund details if they do not make a choice

- Provide employees’ TFNs to their funds.

- Set up your systems to pay super contributions electronically to the right fund.

If you pay extra super for an employee:

- under a salary sacrifice agreement, you must set up the arrangement for the employees’ future earnings, document the arrangement and use a complying fund.

- you must report the amounts being made to the employee’s fund.

Salary Sacrifice Agreements

To create an effective salary sacrifice arrangement, you must:

- set up the arrangement for employees’ future earnings

- document the arrangement

- use a complying fund.

Set Up The Arrangement For Employees’ Future Earnings

The arrangement must be set up for your employee’s future earnings. It can’t include previously earned or accrued:- salary, wages or entitlements

- annual or long service leave.

Document The Arrangement

You and your employee must prepare and sign a document that states the terms of the salary sacrifice arrangement. If you don’t have this documentation, it may be difficult to establish the facts of your arrangement.

Employees can renegotiate the arrangement at any time, within the terms of their employment contract or industrial agreement. If your employee has a renewable contract, you can renegotiate the salary sacrifice amount before the start of each renewal.

Use A Complying Fund

The salary sacrifice amount must be contributed to a complying fund for the period of the arrangement.

Contributions can’t be accessed until the employee satisfies a condition of release, such as reaching retirement age.

Report The Amounts

Reportable employer super contributions (RESC) are not included in your employee’s assessable income. They do not affect the way you calculate super contributions for your employees.

The following employer super contributions are reportable:- additional contributions as part of an employee’s individual salary package

- additional contributions under a salary sacrifice arrangement

- pre-tax amounts paid to an employee’s super fund at the employee’s direction, such as directing an annual bonus into super.

You must report extra contributions if:

- your employee can influence the rate or amount of super you contribute for them; and

- the contributions are in addition to the compulsory contributions you must make under

- super guarantee

- a collectively negotiated industrial agreement

- the rules of a super fund

- federal, state or territory law.

The extra contributions are reportable super contributions for employees, unless you show that:- the extra contributions are made for administrative simplicity

- a documented policy is in place that does not allow an employee to influence the contributions you make on their behalf.

Need help with your business. Speak with the Newcastle Business Accountants Leenane Templeton. Contact us today.

Disclaimer for External Distribution Purposes:

The information contained in this publication is for general information purposes only, professional advice should be obtained before acting on any information contained herein. The receiver of this document accepts that this publication may only be distributed for the purposes previously stipulated and agreed upon at subscription. Neither the publishers nor the distributors can accept any responsibility for loss occasioned to any person as a result of action taken or refrained from in consequence of the contents of this publication. -

Super Guarantee Increasing to 10.5%

From 1st July 2022, those who receive employer super will receive a small increase in their superannuation contributions.

The government legislated an increase in the amount of super that employers have to pay from 9% up to 12% (introduced initially in 2013). This stalled for several years at 9.5% (the super guarantee rate from 2014-2021) until it increased again to 10% last year. At this stage, there seems to be no more stalling until the increase reaches 12%.

When the superannuation guarantee was first introduced in 1992, the rate was set at 3% of your income and was introduced in lieu of a nationwide wage increase. In effect, employees were paying their own super out of forgone wage increases. Nowadays, the increase in superannuation is not being matched by a decrease in your wages.

There is little doubt though, that increasing everyone’s wages by half a per cent would impact on demand for wages. Theoretically, this should lead to a drop in employment numbers/real wages. As employment is currently at a higher rate, this is likely to be an impost (compulsory payment) that employers will have to bear. If you are currently in an employer position, you can expect your wages bill to be higher next year on top of any pay rises that you will give to your staff.

In an employee’s position, however, the only difference that you may notice is a slight increase in the amount of money contributed to your super. This may be a good time to conduct a full review of your super.

Is it with the right fund? Have you got the correct amount of life insurance? Are you in the right investment portfolio? Current legislation should see the rate of superannuation guarantee increase by half a per cent each year until it reaches 12% in the 2025-26 financial year (where it is legislated to remain). With this three per cent increase, it’s believed that people should be able to retire with around a third more of their superannuation (which should mean less reliance on government-funded pensions).

For help with your business or personal finances contact the LT team.

-

Preparing For Your Rental Property’s Tax Deductions

Property is a solid investment opportunity for those looking to increase their financial security.

If you are a landlord, you may be looking for ways to reduce your tax liability this year. This may assist you in turning your property’s cash flow from a negative into a positive.

However, there are limitations to many of the tax deductions that may be available to you, which you need to be aware of.

This includes the fact that you may only claim deductions on your property during the periods in which it was tenanted or genuinely available for rent. You will also only be able to claim the portion of an expense that was used for business purposes and must keep records to prove these expenses.

With that in mind, here is a list of the main tax deductions that landlords should bear in mind when tackling their income tax returns:

Maintenance & Repairs

One of the key deductions that landlords often come into strife with the ATO is to do with maintenance and repairs conducted to the property.

Repairs can be claimed as an immediate deduction if they relate directly to wear and tear (e.g replacing broken tiles after a storm with professional help). You will need to also understand the difference between renovations and repairs. This is because there are different tax treatments to renovations and repairs, and getting the two confused can be costly.

However, if you were to replace an appliance, you would need to claim the cost as a depreciation deduction over the course of an asset’s lifespan. Or, if you were to make an upgrade (such as replacing an old fence or installing new carpets) to increase the value of the property, you will need to claim these costs as a capital works deduction at 2.5% a year for 40 years.

If your rental property was affected by recent flooding events across NSW and Queensland, you may be able to claim the repairs required to make the property habitable again as a tax deduction. This should be discussed with your accountant, however, as it may be tricky to determine the extent of these deductions.

Rental Advertising Costs

It’s a common saying: you have to spend money to make money. So if you have spent money on marketing your property using online or print media, brochures and signs, you can claim these advertising expenses against your income in the same year that you paid for them.

Loan Interest

You can claim the interest charged on a loan for an investment property and any bank fees for servicing the loan. You cannot however claim your repayments on the principal sum of the loan, nor claim interest on the entire size of the loan if you refinanced a portion of the loan for private purposes (regardless of whether equity in an investment property was used as security in that loan. And remember that it is the interest on a loan used to buy your investment property, it doesn’t matter what security you have used. Borrowing against your investment property to pay for a holiday does not come with tax-deductible interest.

Council Rates & Strata Fees

Council rates can be deducted in the year that they are paid, but can only be claimed for the periods in which the house was being rented out.

If your property is on a strata title (such as an apartment block or eligible townhouses), you can claim the cost of body corporate fees.

Building Depreciation

Depending on when your investment property was built, you may be able to claim a deduction on the depreciation of the building’s structure and any renovations you make to the property.

Pest Control

Either the landlord or the tenant can claim an immediate deduction for the hire of a pest control professional.

Insurance

You can claim the cost of insuring a rental property. This may be especially important to note for those who have flood-affected properties, or whose insurance in the area that their property is has increased in cost as a result.

Chat to the LT tax advisors to help with your tax this year.

-

Essential Record-Keeping At Year-End For Your Business

It may seem like the importance of record-keeping is overly stressed by us, but it’s a critical part of the wrap-up of the year-end.

Good record-keeping makes it easier to meet your tax obligations, manage your cash flow and make sound business decisions going forward. Put the hard work in at the end of the financial year to get your business organised and allow you to work smarter in the year ahead.

Essential business records that must be kept include:

Expense Or Purchase Records

You must keep records of all business expenses, such as receipts, tax invoices, cheque book receipts, credit card vouchers and diaries to record small cash expenses.

Year-end Records

These records include lists of creditors or debtors and worksheets to calculate depreciating assets, stocktake sheets and capital gains tax records.

Income & Sales Records

You must keep records of all income and sale transactions such as tax invoices, receipt books, cash register tapes and records of cash sales.

Bank Records

Documents such as bank statements, loan documents and bank deposit books need to be kept in preparation for your tax return.

Fuel Tax Credits

To claim fuel tax credits for your business, records must show that you acquired the fuel, used it in your business, and applied the correct rate when calculating how much you are eligible to claim.

Payments To Employees & Contractors

Records of your workers need to be kept, including tax file numbers, withholding declaration forms, contributions to their superannuation, wages and any other payments made to them.

By law, business records must be kept for a minimum period of five years for sole traders and individuals and seven years for companies’ and payroll transactions after the record is created, updated, the transaction is completed or the return in which they were included was lodged, whichever is the latter.

Records can be kept electronically or on paper, must be in English or in a form that can be easily converted, and thoroughly explain all transactions. Failure to keep the correct tax records can incur penalties from the ATO.

By maintaining consistent records throughout the year of your major and minor expenses, you will be in a better position to face the end of the financial year. Take the stress and hassle out of this tedious process by coming to Leenane Templeton with all of the information that is needed for your tax returns to be completed. Contact us

-

Superannuation Strategies To Employ Before The EOFY

With superannuation being the key to a comfortable retirement, here are some of the strategies to consider that could help with streamlining your finances (while also taking into account some considerable tax breaks).

Concessional Contributions

Also known as the before-tax contributions, these are the funds that go into your super account from your income before tax. These can include

• Employer contributions

• Salary sacrifice payments

• Personal contributions (which can be claimed as a tax deduction).The concessional contributions cap is $27,500 for all ages for the 2021-22 financial year. Your cap may be higher if you did not use the full amount of your cap in previous years. This is called the carry-forward of unused concessional contributions.

Bear in mind that if your combined income and concessional contributions are more than $250,000 in total, you may have to pay extra tax. This is something to consider if you are looking to make personal contributions for the sake of the tax deduction.

Non-Concessional Contributions

Before-tax contributions are not the only way to top up your super account. Non-concessional contributions are made into your super fund from after-tax income. They include contributions made by you or your employer on your behalf from aftertax income, contributions made by your spouse to your super fund, or personal contributions not claimed as an income tax deduction.

For the 2021-22 financial year, the non-concessional contributions cap is being increased to $110,000. If you contribute more than this, you may have to pay extra tax on this.

Your own cap may be different from others though, as it could be:

• Higher, if you are able to use the bring-forward arrangements

• Nil, if your total super balance is greater than or equal to the general transfer balance cap ($1.7 million from 2021-22)Changes Coming Into Effect 1 July 2022

Though the recent Budget announcements for superannuation only covered the reduction to the minimum annual drawdown amounts for superannuation pensions and annuities, that doesn’t mean that there aren’t other changes still to come into effect from last year’s announcements. Be mindful of the following when planning your superannuation strategies for next year:

• Bring-forward non-concessional cap extended to anybody under 75 (subject to Total Superannuation Balance

• Work test requirements were abolished for 67-74-yearolds in respect of making or receiving personal and salary sacrificed contributions.

• The SG rate is set to increase to 10.5% (up from the current 10%), as applicable to an employee’s (and some contractors’) ordinary time earnings.

• $450 per month income threshold abolished for SG contributions – those earning below this amount may now be eligible for the superannuation guarantee.

• Reduction to age 60 (down from 65) for the home downsizer contribution scheme

• Increase to voluntary contribution release amounts under the first home super saver scheme from $30,000 to $50,000For help with you superannuation or financial planning please contact our team of LT advisors.

-

2022 End Of Financial Year Checklist

Maximise your tax deductions for the 2021-22 financial year by conducting a thorough review of your records. But to do that, you need to know where to start. Here are some of our top tips for businesses and individuals when it comes to year-end tax planning.

For Businesses

Temporary Full-Expensing

Any asset purchased between 7.30pm AEDT 6 October 2020 to 30 June 2022 may be written off by a small business under the instant asset write-off. This even applies second-hand assets (where your turnover is under $50 million). Purchasing later in the tax year (June) as opposed to early in the new year (July) can give you a benefit far sooner in the tax savings that are made on that purchase.

Bad Debts

Bad debts incur a significant cost to all businesses that sell on credit. There is no sense in paying tax and GST on sales where payment will not be received, which is why reviewing if your business has any bad debts attached to it before the end of the year is important. Claiming a tax deduction for bad debts is surrounded by complicated rules, so it may be best to speak with a professional (like us) for further information and assistance.

Small Business CGT Concessions

Individuals operating a small business may be eligible for capital gains tax (CGT) concessions on the sale of business assets. The small business CGT concessions are available to business taxpayers with an aggregated turnover of less than $2 million or on business assets less than $6 million. Review your potential concessions for this financial year to receive the benefits of tax relief or contribute to your retirement savings through the sale of a business. Careful planning around the Small Business Concessions could potentially save hundreds of thousands of dollars in tax on the eventual sale of your business.

Stocktake

The year-end stocktake should involve a review of all trading stock and a decision made about its value from both a tax and commercial perspective. Obsolete, slow-moving or damaged stock should be identified by 30 June and disposed of for income purposes in order to receive a deduction.

Pay Quarterly Super

In order to qualify for a tax deduction for the 2021-22 financial year, Super Guarantee contributions must be paid by 30 June 2022. Some clearing houses can take more than a week to submit the payment to the super fund, but the fund must receive the contribution before the deadline. To keep on top, the best practice may be to pay before 20 June (to allow the extra time for the clearing houses to process the payment.

For Individuals

Work From Home Deductions

If you’ve been working from home during lockdowns or as a result of the pandemic’s effects, the ‘shortcut method’ is available to claim running expenses at the rate of 80c per hour worked. You will not be able to claim using other methods though, and will not be able to claim on asset depreciation.

LMITO Offset

If you’re within the Low & Middle-Income Tax Brackets for the offsets, you may be eligible for additional tax relief on your income tax return. We can assist you in checking if you will be able to claim this or not.

Depositing Contributions

Any contributions that have been recorded for your SMSF need to be deposited into the fund’s bank account by no later than 30 June. This is especially important where members have reported concessional or non-concessional contributions on their tax returns. But remember that you can;t claim the tax deduction until you have lodged your notice of intent to claim a tax deduction and have received an acknowledgement back from the fund. No early lodgements if you have made a contribution to super.

We Are Here To Help

This guide is merely meant to provide you with a starting point for identifying the areas that might have a significant impact on your personal and business planning. We’re always glad to consult with you on such matters and advise in any way that we can.

For further help contact Leenane Templeton.

-

Trust Planning This Year Needs To Be Done Carefully

In order to prepare your trust for the end of the financial year, there are multiple obligations that you need to fulfil as a trustee. Planning for your trust’s future is just as important as tax planning or business planning, so it’s encouraged that you take an active role.

Trust Deed

Make sure that there is a complete original copy of the trust deed, including any amendments. You will need to be sure that any resolution that is made to distribute the income from the trust or the capital is consistent with the terms of the deed. A lost trust deed can cost well over $10,000 to rectify.

Trust Distributions

The simplest way to look at trust distributions is to understand that this process is about working out who is getting what and when from the trust.

Generally, discretionary trusts (and some fixed trusts) are required to prepare and execute distribution minutes prior to 30 June for each financial year. This is to explain in detail how the income of the trust will be distributed to beneficiaries for the relevant financial year and must detail any use of income streaming. These minutes must be prepared in accordance with the trust deeds. Failure to do these resolutions by 30th June will result in the trust paying 47% tax on ALL of its earnings.

When preparing the trust distribution minutes, it may be an idea to retain a nominal amount in the trust for the 30 June 2022 income year. This will assist with generating a notice of assessment for the trust and effectively limiting the amendment period to 4 years (or 2 years for trusts that are considered a small business entity) from the date of that notice.

Broadly, the amendment period is a period of time that the ATO and taxpayer are able to review and amend tax forms to where their taxable income needs to be changed. The period is determined from the date of the relevant notice of assessment.

Where there is no retention of income, trusts are generally not taxable and therefore do not receive notices of assessment. As such, without completing the distribution minutes and retaining a nominal amount in the trust by 30 June 2022, the amendment period will be greater than 4 or 2 years.

Compliance Concerns

A commonly recommended structure for investment and business, family trusts income distributions are a concern for the Australian Taxation Office (ATO) when it comes to compliance. Recent rulings around trust distributions could complicate the way your trusts are operated and structured and will come into effect on 1 July 2022.

Work together with Leenane Templeton to ensure that your trust is compliant with their requirements and that you have met your obligations as a trustee. This is the easiest way to approach your trust planning at the end of the year. Contact us today.

-

Why Is End Of Year Planning So Important?

Benjamin Franklin once famously said, “if you fail to plan, you are planning to fail”. He may not have been referring specifically to businesses but it is an apt statement for individuals and businesses alike. We all need to plan where we are going. It could be as simple as planning a holiday or it could be to do with the next ten years of our business.

Business planning is a key element to success. Businesses with a formal business plan perform far better than those that don’t, and with good reason. If you know where you want to get to you, there is far more chance of getting there.

For the most simple of plans for a business, why not prepare a budget for 2023? Each month thereafter you can compare your actual performance to that of the budget. You will probably find that by preparing the budget you will find areas where you can save expenses. You will also know on a monthly basis how you are travelling, and be able to adapt as needed.

You could also consider a full planning session with your team leading up to the end of the financial year. Bring the team together, find a facilitator and brainstorm all of the ideas that you could use to grow your business. Your team will be more engage when they have input into what your growth activities will be.

Don’t forget the business formula – that your total revenue is your number of customers times the number of sales per customer by the average value per sale. A 10% increase in each could drive your growth by more than 30%.

If you would like to explore your options for planning next year, give us a call. There is plenty that we can tackle together for your business chat with your Leenane Templeton accountant or contact us here.

-

Last Chance To Apply As COVID-19 Tax Deduction Deadlines Approach

Tax deductions introduced by the Australian Taxation Office to lessen the impact of COVID-19 are approaching the end of their eligible timeframe. To ensure that you or your business do not miss out, here are some of the deductions you could claim at the end of this financial year (if eligible).

Loss-Carry Back Rules

Eligible businesses with an aggregated turnover of less than $5 billion or corporate tax entities that meet an alternative $5 billion total income test are able to use the temporary fill-expensing measure again this year. This will allow them to deduct the full cost of eligible depreciating assets acquired from 6 October 2020 and first used or installed ready for use by 30 June 2023. The original deadline of 30 June 2022 was extended for an additional year, so make sure to make use of this in your business!

Shortcut Method

If you have had to work from home over the last year between 1 July 2021 to 30 June 2022, you can claim a deduction for working from home.

This is to address expenses that you may have had to make in order to work from home, such as paying for electricity or equipment to work from home. These expenses cannot have been paid by your employer, you need to have paid for them yourself.

You can claim $0.80 for every hour that you worked from home, but you are not able to claim for anything else if using this method.

To claim this, you need to:

- keep a record of how many hours you worked from home

- work out your deduction amount

- write the deduction amount in your tax return in the ‘Other work-related expenses’ section

- write ‘COVID-19 hourly tax rate’ in your tax return.

If you are consulting with a registered tax agent like Leenane Templeton for your return, they may recommend this as your best course of action.

For more information please feel free to contact the LT team.

-

Your Work-Related Tax Deduction Checklist

Your Work-Related Tax Deduction Checklist For This Year’s Tax Return Made Easy

The end of the financial year is coming up (30 June), and you may be looking for ways in which you could make tax savings in this year’s tax return. This could be through tax deductions, expenses that you could make now for your work purposes or even with tax offsets introduced by the government. Whatever your tax situation, we’re equipped and ready to help you navigate the tricks and traps of income tax returns.

Upon completing a tax return, individuals are entitled to claim deductions for expenses that are directly related to their income. These can come in a variety of forms, but must usually be work-related to be claimable.

There are three requirements individuals must meet to be able to claim a work-related deduction:

– the individual must have spent their money and not be reimbursed for it

– the expense must be related to their job and;

– there must be a record, like a receipt, to be able to prove it.

If an expense was for work and private purposes, individuals can claim a deduction for the work-related portion.Here are some common types of deductible expenses taxpayers like employees and rental property owners can claim this financial year:

Home Office Expenses

The past year may have seen you working more from home or remotely than ever before, and setting up a home office may have incurred a number of additional expenses. Some of the expenses that you may be able to claim as tax deductions include:

– Phone and internet expenses

– Computer consumables (such as printer paper and ink) and stationery

– Home office equipment (such as computers, phones, printers, furniture, etc).

With home office equipment, you may be able to claim either:

– the full cost of the items (if less than $300 in value) or

– The decline in value (also known as depreciation) for items over $300.

Unless you meet very specific requirements, you probably will not be able to claim for home expenses, such as mortgage interest, rent and rates, or the cost of general household items.

If you plan to use the temporary ATO approved ‘shortcut method’ (80 cents per hour for all additional running expenses) to claim your deductions, you cannot claim any other expenses for working from home for that period. If you purchased a desk to use when working from home, for example, you cannot claim a deduction for that separately as it is covered by the 80 cents per hour work rate. The deadline for this method of calculation is 30 June 2022 (unless it is extended).

Clothing Expenses

Individuals can make a claim for work-related clothing expenses including compulsory, non-compulsory and registered uniforms, occupation-specific and protective clothing, and expenses associated with work-related clothing, such as dry cleaning, laundry and repair expenses.

Self-education Expenses

Individuals can prepay self-education items before the end of the income year, including:

– course fees (not HECS-HELP fees), student union fees and tutorial fees

– stationery and textbook purchases

Other Work-related Expenses

Individuals can prepay the following expenses before 1 July 2022:

– union fees seminars and conferences

– subscriptions to trade, professional or business associations

– subscriptions to magazines and newspapers

If you are looking for assistance in working out potential expenses that you could incur prior to the end of the financial year, have queries about your claims or just want to prepare for 30 June 2022, start a conversation with us now. We are tax planning professionals ready and willing to help.Contact us today

-

Reminder: Director Identification Number for Business

As of 5 April 2022, new Directors will need to have applied for their Director Identification Number (DIN) prior to their appointment to the position.

Existing directors were required to obtain a DIN prior to the end of the transitional period (30 November 2022), whereas directors of Indigenous Corporation have until 30 November 2023. Failure to do so could result in penalties for non-compliance.

What Is A Director Identification Number?

Previously a company or business was registered through ASIC, where a Tax File Number and an Australian Business Number would be required. These are obtained through the Australian Taxation Office (ATO) and are a critical part of setting up a business or company.

Introduced in November 2021, there will be an additional step introduced in the registering of a company, involving a Director Identification Number (DIN). This director identification number is a unique identifier that a director will apply for once and keep forever.

They were brought in as a part of a broader regulatory strategy to address the issue of phoenixing – this is where controllers of a company deliberately avoid paying liabilities by shutting down indebted companies and transferring assets to another company. DINs are recorded in a database to be administered and operated by the Australian Tax Office and are made available to the public.

The ATO has the power to provide, record, cancel and re-issue a person’s DIN. A DIN will be automatically cancelled if the individual does not become a Director within 12 months of receiving the DIN.

Who Does A DIN Apply To?

Director ID only applies to companies and corporate bodies registered under the Corporations Act and CATSI Act.

Director ID does not apply to sole traders, partnerships or trusts unless the trust has a corporate trustee.

Deadlines For Applying For A DIN

When the announcement of DINs was made in April 2021, there were set deadlines in place for those involved in profit and not-for-profit entities, as well as for Indigenous Directors. As of 5 April 2022, those deadlines have changed.

For for-profit- entities, the deadline for applying for a DIN under the Corporations Act must be done before your appointment as a director.

For non-profit entities (including those entities registered under the ACNC Act as either private or public companies), you also need to have applied for your DIN before you are appointed as a director. For new directors of Indigenous Corporations, the same requirements for applying are advised (prior to appointment).

How To Apply For A DIN

All directors must apply for their own DIN. This cannot be done by a third part, unless it can be proven to the Registrar that the director is unable to make the application on their own behalf (such as suffering some sort of incapacity, etc).

There are three ways to apply for a DIN: Online application via the myGovID app. This is different to myGov and is the quickest way to obtain a DIN.Phone application.Paper application (which is the slowest process).

These methods require proof of identity documentation, however, you may be able to use certified copies (witnessed by a Justice of the Peace) if you are using the paper application.

Should you have any queries with regards to your DIN please contact your LT accountant on 02 4926 2300 -

Inflation – What is it and how does it affect you?

Inflation is a hot topic at the moment. But what exactly is it, and how does it affect you and your money?

Inflation is making news daily through wage inflation, energy inflation, food inflation, fuel inflation… and not just in Australia, but in many other countries too. In simple terms, inflation means that the prices of everyday things are rising. Why does this matter? It means that unless our incomes rise in line with inflation, our money doesn’t go as far, and we might find it more difficult to buy the kinds of things that we’re used to having.

How high is inflation?

According to the most commonly used measure of inflation in Australia, the Consumer Price Index (CPI), inflation increased by 0.8% in the July to September 2021 quarter and rose 3% over the 12 months to September 2021.Why does inflation happen?

There are two main causes of inflation:

- “Cost push inflation” is where the costs of producing goods or services goes up, and so price rises are passed onto customers.

- “Demand pull inflation” is when something is so popular that the supplier can’t meet the demand. Prices go up to reflect the lack of supply.

How is inflation measured?

The official Australian inflation measures come from the Australian Bureau of Statistics (ABS), which tracks prices of a ‘basket’ of commonly purchased goods and services. This is supposed to represent the spending of the average Australian household. As people’s buying habits change, so do the goods and services that the ABS tracks.

For example, in recent years, the ABS has added streaming services, ride sharing and smart phones to the CPI basket and removed items such as DVD hiring, cassette tapes and VCRs from the basket to more adequately represent the average household expenditure.

How is inflation controlled?

The Reserve Bank of Australia (RBA) has a specific responsibility for low and stable inflation, full employment, and promoting the general welfare of the Australian people. The government has set a target of 2-3% for inflation, on average over time.What does rising or high inflation mean for:

■ your spending. Rising prices of goods and services will mean that unless your income rises too, you will find it more difficult to afford the things you normally buy. Sharp movements in the rate of inflation are not helpful either, because they make it difficult for people to plan their spending. For example, rising inflation can trigger “buy now while stocks last” behaviour.

■ your savings. If your savings don’t grow at a rate at least equal to inflation your wealth is shrinking. For example, inflation is now running at 3%, but cash in a current account is likely to earn less than 0.10% interest. Its value is being quietly eroded with every day that passes. This effect of inflation is easier to see by looking back in history.

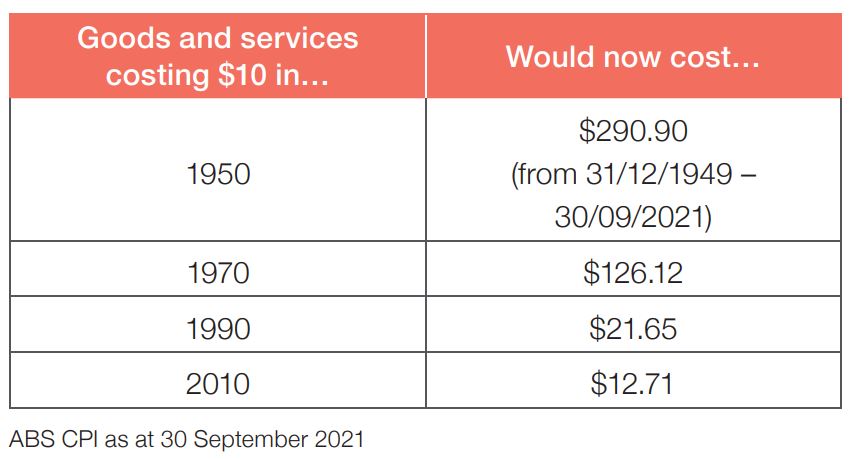

The following table shows how much you would need to spend today to equal $10 spent in each of the following years:

■ your loans. The RBA tends to use interest rates as its primary tool to control inflation. As inflation rises, the RBA tends to be more willing to raise interest rates – meaning mortgages, loans and credit cards can become more expensive.

■ your investing. When inflation is rising, or already high, holding assets such as shares, property and bonds (or even foreign currency) can be more attractive than keeping your cash in a bank account (because, as inflation rises, the value of cash tends to fall relative to other types of assets) – but shifts in inflation and interest rate expectations can also spook investors, creating volatility and unpredictability in asset prices.

If you have any questions, please speak with a LT Advisor.

-

Federal Budget Highlights 2022-2023

We have pleasure in enclosing a summary of the tax, superannuation and social security highlights from the Federal Government’s 2022/23 Budget.

Addressing Cost of Living Pressures – temporary reduction in fuel excise

Global oil prices have risen significantly since the Russian invasion of Ukraine. The Government will help reduce the burden of higher fuel prices at home by halving the excise and excise-equivalent customs duty rate that applies to petrol and diesel for 6 months. The excise and excise-equivalent customs duty rates for all other fuel and petroleum-based products, except aviation fuels, will also be reduced by 50 per cent for 6 months. The Government is responding in a temporary, targeted and responsible way to reduce cost of living pressures experienced by Australian households and small businesses.

The measure will commence from 12.01am on 30 March 2022 and will remain in place for 6 months, ending at 11.59pm on 28 September 2022. Under the measure, existing policy settings for fuel excise and excise-equivalent customs duty, including indexation in August, will continue but on the basis of the halved rates. At the conclusion of the 6 month period the excise and excise-equivalent customs duty rates will then revert to previous rates, including indexation that would have occurred on those rates during the 6 month period.

The rate of excise and excise-equivalent customs duty currently applying to petrol and diesel is 44.2 cents per litre. This measure will halve the rate on petrol and diesel to 22.1 cents per litre from 30 March 2022, with the price faced by consumers expected to be reduced by a larger magnitude given GST will be levied on the lower excise rate.

The Australian Competition and Consumer Commission will monitor the price behaviour of retailers to ensure that the lower excise rate is fully passed on to Australians.

This targeted measure to provide temporary relief from fuel price pressures will be legislated to end on 28 September 2022.

This measure is estimated to decrease receipts by $5.6 billion, and decrease payments by $2.7 billion over the forward estimates period.

Source: Budget Paper No 2, p 15.

Cost of living tax offset

The Government will increase the low and middle income tax offset (LMITO) for the 2021-22 income year. LMITO is targeted at low- and middle-income earners that are most susceptible to cost of living pressures. The Government is responding in a temporary, targeted and responsible way to reduce cost of living pressures experienced by Australian households.

The LMITO for the 2021-22 income year will be paid from 1 July 2022 when Australians submit their tax returns for the 2021-22 income year. This proposal will increase the LMITO by $420 for the 2021-22 income year. This increases the maximum LMITO benefit in 2021-22 to $1,500 for individuals and $3,000 for couples.

Other than those that do not require the full offset to reduce their tax liability to zero, all LMITO recipients will benefit from the full $420 increase. All other features of the current LMITO remain unchanged. Consistent with the current LMITO, taxpayers with incomes of $126,000 or more will not receive the additional $420.

This measure is estimated to decrease receipts by $4.1 billion over the forward estimates period.

This measure builds on the 2021-22 Budget measure titled Retaining the low and middle income tax offset for the 2021-22 income year.

Source: Budget Paper No 2, p 16.

COVID-19 Response Package – making COVID-19 business grants non-assessable non-exempt

The Government has extended the measure which enables payments from certain state and territory COVID-19 business support programs to be made non-assessable non-exempt (NANE) for income tax purposes until 30 June 2022. This measure was originally announced on 13 September 2020.

In recognition that NANE tax treatment is only to be provided in exceptional circumstances, eligibility is limited to COVID-19 grant programs directed at supporting businesses that are the subject of a public health directive applying to a geographical area in which the businesses operate and whose operations have been significantly disrupted as a result of the public health directive. Consistent with this, the Government has made the following state and territory grant programs eligible for this treatment since the 2021-22 MYEFO:

• New South Wales Accommodation Support Grant

• New South Wales Commercial Landlord Hardship Grant

• New South Wales Performing Arts Relaunch Package

• New South Wales Festival Relaunch Package

• New South Wales 2022 Small Business Support Program

• Queensland 2021 COVID-19 Business Support Grant

• South Australia COVID-19 Tourism and Hospitality Support Grant

• South Australia COVID-19 Business Hardship Grant.

This measure is estimated to result in an unquantifiable decrease in receipts over the forward estimates period.

Source: Budget Paper No 2, p 17.

COVID-19 Response Package – tax deductibility of COVID-19 test expenses

The Government will ensure that the costs of taking a COVID-19 test to attend a place of work are tax deductible for individuals from 1 July 2021. In making these costs tax deductible, the Government will also ensure fringe benefits tax (FBT) will not be incurred by businesses where COVID-19 tests are provided to employees for this purpose.

This measure is estimated to result in a significant but unquantifiable decrease in receipts over the forward estimates period.

Further information can be found in the media release of 8 February 2022 issued by the Minister for Housing and Assistant Treasurer.

Source: Budget Paper No 2, p 18.

Deferral of Shadow Economy – strengthening the Australian Business Number system measure

The Government will defer the start date of the Black Economy – strengthening the Australian Business Number (ABN) system measure, announced in the 2019-20 Budget, by 12 months to assist with integration into the Australian Business Registry Services (ABRS).

This measure is estimated to decrease receipts by $5.0 million over the forward estimates period.

Source: Budget Paper No 2, p 18.

Digitalising trust income reporting and processing

The Government will digitalise trust and beneficiary income reporting and processing, by allowing all trust tax return filers the option to lodge income tax returns electronically, increasing pre-filling and automating ATO assurance processes.

The measure will commence from 1 July 2024, subject to advice from software providers about their capacity to deliver.

Trust income reporting and assessment calculation processes have not been automated to the same extent as individual or company tax returns, resulting in longer processing times and limited pre-filling opportunities. This measure will reduce the compliance burdens on taxpayers, reduce processing times and enhance ATO processes.

The Government will consult with affected stakeholders, tax practitioners and digital service providers to finalise the policy scope, design and specifications.

This measure is estimated to result in an unquantifiable impact on receipts over the forward estimates period.

Source: Budget Paper No 2, p 18, 19.

Employee Share Schemes – expanding access and further reducing red tape

The Government will expand access to employee share schemes and further reduce red tape so that employees at all levels can directly share in the business growth they help to generate.

Where employers make larger offers in connection with employee share schemes in unlisted companies, participants can invest up to:

• $30,000 per participant per year, accruable for unexercised options for up to 5 years, plus 70 per cent of dividends and cash bonuses; or

• any amount, if it would allow them to immediately take advantage of a planned sale or listing of the company to sell their purchased interests at a profit.

The Government will also remove regulatory requirements for offers to independent contractors, where they do not have to pay for interests.

This measure is estimated to result in an unquantifiable impact on receipts over the forward estimates period.

Source: Budget Paper No 2, p 19.

Modernisation of pay as you go (PAYG) instalment systems

The Government will enable companies to choose to have their pay as you go (PAYG) instalments calculated based on current financial performance, extracted from business accounting software, with some tax adjustments. This will support business cash flow by ensuring instalments reflect current performance.

The Government will consult with affected stakeholders, tax practitioners and digital service providers to finalise the policy scope, design and specifications of this measure.

Subject to advice from software providers about their capacity to deliver, it is anticipated that systems will be in place by 31 December 2023, with the measure to commence on 1 January 2024, for application to periods starting on or after that date.

This measure will improve alignment between PAYG instalment liabilities and profitability, and support companies in managing cash flows.

This measure is estimated to result in an unquantifiable impact on receipts over the forward estimates period.

Source: Budget Paper No 2, p 21.

Personal Income Tax – increasing the Medicare levy low-income thresholds

The Government will increase the Medicare levy low-income thresholds for seniors and pensioners, families and singles from 1 July 2021. The increase in thresholds takes account of recent movements in the consumer price index so that low-income individuals continue to be exempt from paying the Medicare levy.

The threshold for singles will be increased from $23,226 to $23,365. The family threshold will be increased from $39,167 to $39,402. For single seniors and pensioners, the threshold will be increased from $36,705 to $36,925. The family threshold for seniors and pensioners will be increased from $51,094 to $51,401. For each dependent child or student, the family income thresholds will increase by a further $3,619 instead of the previous amount of $3,597.

This measure is estimated to decrease receipts by $90.0 million over the forward estimates period.

Source: Budget Paper No 2, p 24, 25.

Small Business – skills and training boost

The Government is introducing a skills and training boost to support small businesses to train and upskill their employees. The boost will apply to eligible expenditure incurred from 7:30pm (AEDT) on 29 March 2022 (Budget night) until 30 June 2024.

Small businesses (with aggregated annual turnover of less than $50 million) will be able to deduct an additional 20 per cent of expenditure incurred on external training courses provided to their employees. The external training courses will need to be provided to employees in Australia or online, and delivered by entities registered in Australia.

Some exclusions will apply, such as for in-house or on-the-job training and expenditure on external training courses for persons other than employees.

The boost for eligible expenditure incurred by 30 June 2022 will be claimed in tax returns for the following income year. The boost for eligible expenditure incurred between 1 July 2022 and 30 June 2024, will be included in the income year in which the expenditure is incurred.

This measure is estimated to decrease receipts by $550.0 million, and increase payments by $7.0 million over the forward estimates period.

Source: Budget Paper No 2, p 26, 27.

Small Business – technology investment boost

The Government is introducing a technology investment boost to support digital adoption by small businesses. The boost will apply to eligible expenditure incurred from 7:30pm (AEDT) on 29 March 2022 (Budget night) until 30 June 2023.

Small businesses (with aggregated annual turnover of less than $50 million) will be able to deduct an additional 20 per cent of the cost incurred on business expenses and depreciating assets that support their digital adoption, such as portable payment devices, cyber security systems or subscriptions to cloud-based services.

An annual cap will apply in each qualifying income year so that expenditure up to $100,000 will be eligible for the boost.

The boost for eligible expenditure incurred by 30 June 2022 will be claimed in tax returns for the following income year. The boost for eligible expenditure incurred between 1 July 2022 and 30 June 2023 will be included in the income year in which the expenditure is incurred.

This measure is estimated to decrease receipts by $1.0 billion, and increase payments by $7.2 million over the forward estimates period.

Source: Budget Paper No 2, p 27.

Smarter reporting of Taxable Payments Reporting System data

The Government will allow businesses the option to report Taxable Payments Reporting System data (via accounting software) on the same lodgment cycle as their activity statements.

Subject to advice from software providers about their capacity to deliver, it is anticipated that systems will be in place by 31 December 2023, with the measure to commence on 1 January 2024, for application to periods starting on or after that date.

This measure will increase the accuracy and timeliness of reporting while lowering compliance costs for taxpayers.

The Government will consult with affected stakeholders, tax practitioners and digital service providers to finalise the policy scope, design and specifications of the measure.

This measure is estimated to result in an unquantifiable impact on receipts over the forward estimates period.

Source: Budget Paper No 2, p 28.

Supporting Retirees – extension of the temporary reduction in superannuation minimum drawdown rates

The Government has extended the 50 per cent reduction of the superannuation minimum drawdown requirements for account-based pensions and similar products for a further year to 30 June 2023.

The minimum drawdown requirements determine the minimum amount of a pension that a retiree has to draw from their superannuation in order to qualify for tax concessions.

Given ongoing volatility, this change will allow retirees to avoid selling assets in order to satisfy the minimum drawdown requirements.

This measure is estimated to decrease receipts by $50.0 million and increase payments by $2.8 million over the forward estimates period.

Source: Budget Paper No 2, p 28.

Tax Integrity – extension of the Australian Taxation Office (ATO) Tax Avoidance Taskforce on multinationals, large corporates and high wealth individuals

The Government will provide $325.0 million in 2023-24 and $327.6 million in 2024-25 to the ATO to extend the operation of the Tax Avoidance Taskforce by 2 years to 30 June 2025.

The Taskforce was established in 2016 to undertake compliance activities targeting multinationals, large public and private groups, trusts and high wealth individuals. It also scrutinises specialist tax advisors and intermediaries that promote tax avoidance schemes and strategies.

The ATO’s total resourcing requirement, including for the delivery of the extension of the Tax Avoidance Taskforce, will be settled as part of the independent review of the ATO’s ongoing resourcing requirement announced as part of the 2021-22 MYEFO measure titled Australian Taxation Office – continuation of compliance programs and independent resourcing review.

This measure is estimated to increase receipts by $2.1 billion, and increase payments by $652.6 million over the forward estimates period.

Source: Budget Paper No 2, p 29.

Varying the GDP uplift factor for tax instalments

The Government has decided to set the GDP uplift factor for pay as you go (PAYG) and GST instalments at 2 per cent for the 2022-23 income year. This uplift factor is lower than the 10 per cent that would have applied under the statutory formula.

The lower uplift rate will provide cash flow support to small businesses, including sole traders, and other individuals with investment income, helping them to invest and grow. Around 2.3 million taxpayers are expected to benefit from this measure.

The 2 per cent GDP uplift rate will apply to small to medium enterprises eligible to use the relevant instalment methods (up to $10 million annual aggregated turnover for GST instalments and $50 million annual aggregated turnover for PAYG instalments) in respect of instalments that relate to the 2022-23 income year and fall due after the enabling legislation receives Royal Assent.

This measure is estimated to have no net impact on receipts, and no net impact on GST payments to the States and Territories over the forward estimates period.

Source: Budget Paper No 2, p 29, 30.

Cost of Living Payment

The Government will provide $1.5 billion in 2021-22 to provide a $250 economic support payment to help eligible recipients with higher cost of living pressures. The payment will be made in April 2022 to eligible recipients of the following payments and to concession card holders:

• Age Pension

• Disability Support Pension

• Parenting Payment

• Carer Payment

• Carer Allowance (if not in receipt of a primary income support payment)

• Jobseeker Payment

• Youth Allowance

• Austudy and Abstudy Living Allowance

• Double Orphan Pension

• Special Benefit

• Farm Household Allowance

• Pensioner Concession Card (PCC) holders

• Commonwealth Seniors Health Card holders

• eligible Veterans’ Affairs payment recipients and Veteran Gold card holders.

The payments are exempt from taxation and will not count as income support for the purposes of any income support payment. A person can only receive one economic support payment, even if they are eligible under 2 or more of the categories outlined above. The payment will only be available to Australian residents.

Source: Budget Paper No 2, p 167.

Affordable Housing and Home Ownership

The Government will increase the number of guarantees under the Home Guarantee Scheme to 50,000 per year for 3 years from 2022-23 and then 35,000 a year ongoing to support homebuyers to purchase a home with a lower deposit. The guarantees will be allocated to provide:

• 35,000 guarantees per year ongoing for the First Home Guarantee (formerly the First Home Loan Deposit Scheme)

• 5,000 places per year to 30 June 2025 for the Family Home Guarantee

• 10,000 places per year to 30 June 2025 for a new Regional Home Guarantee that will support eligible citizens and permanent residents who have not owned a home for 5 years to purchase a new home in a regional location with a minimum 5 per cent deposit.

This will come at a cost of $8.6 million over 4 years from 2022-23 and $138.7 million over 7 years from 2026-27, with $20.5 million per year ongoing from 2033-34.

The Government will also increase the Government guaranteed liability cap of the National Housing and Finance Investment Corporation (NHFIC) by $2.0 billion to $5.5 billion to enable NHFIC to support increased loans through the Affordable Housing Aggregator, which increases support for affordable housing.

This measure builds on the 2021-22 MYEFO measure titled Supporting the Delivery of More Affordable Housing and the 2021-22 Budget measure titled Housing Package.

Source: Budget Paper No 2, p 170.

COVID-19 Economic Support

In addition to the $7.3 billion provided in MYEFO for COVID-19 Business Support Payments, the Government will provide a further $53.9 million in 2021-22 to extend COVID-19 Business Support Payments and access to the Pandemic Leave Disaster Payment. Further information on jointly-funded business support arrangements for all states and territories is provided in Budget Paper 3 – Federal Financial Relations.

This measure builds on the 2021-22 MYEFO measure titled COVID-19 Response Package – COVID-19 Business Support.

Source: Budget Paper No 2, p 171.

Reducing compliance costs for business through enhanced sharing of single touch payroll data

The Government will commit $6.6 million over the forward estimates period for the development of IT infrastructure required to allow the ATO to share single touch payroll (STP) data with State and Territory Revenue Offices on an ongoing basis.

Funding for this measure has already been provided for by the Government.

The funding will be deployed following further consideration of which states and territories are able and willing to make investments in their own systems and administrative processes to pre-fill payroll tax returns with STP data, to reduce compliance costs for businesses.

Source: Budget Paper No 2, p 172.

Small Business Support Package

The Government will provide $25.2 million over 3 years from 2021-22 to deliver initiatives to support small businesses. Funding includes:

• $10.4 million over 2 years from 2022-23 to enhance and redesign the Payment Times Reporting Portal and Register to improve efficiency and reporting

• $8.0 million in 2022-23 to the Australian Small Business and Family Enterprise Ombudsman to work with service providers to enhance small business financial capability

• $4.6 million over 2 years from 2021-22 to support the New Access for Small Business Owners program delivered by Beyond Blue to continue to provide free, accessible, and tailored mental health support to small business owners

• $2.1 million over 2 years from 2021-22 to extend the Small Business Debt Helpline program operated by Financial Counselling Australia to continue to provide financial counselling to small businesses facing financial issues.

Further information can be found in the media release of 13 January 2022 issued by the Acting Minister for Employment, Workforce, Skills, Small and Family Business.

Source: Budget Paper No 2, p 172.

-

It’s Fringe Benefits Tax Time

The end of the FBT year (1 April – 31st March) is fast approaching, and it is a good time to reflect on your FBT plans for the year.

Fringe benefits are benefits that you provide to your staff that fall outside the categories of traditional wages and salaries. Examples of common fringe benefits include cars, low interest or interest-free loans and school fees.

Fringe benefits are taxed differently to income, and business owners should be aware of the relevant compliance issues when negotiating salary packages. The benefits are not subject to income tax. However, the employer must pay fringe benefits tax (FBT). Typically, the employer will reduce the employee’s salary by the amount equivalent to the FBT incurred.

The FBT rate for the year ending 31 March 2021-2022 is 47%.

It is advisable to seek professional guidance before entering into a new salary packaging agreement with an employee. The reason for this is that the calculations surrounding FBT calculations are extremely complex, and you may end up inadvertently disadvantaging them in the process, thereby defeating the purpose of salary packaging.

Contact our FBT accountants today. Call: 02 4926 2300

-

Financial Advice Helps You Achieve More!

Whatever you want to do, you’re more likely to do it with the help of some sound financial advice.

We all have something we’d like to be doing more of. It could be spending more time on hobbies, less time at work and more time raising a family, more time travelling the world or reducing working hours as we get closer to retirement. One thing we all want to make sure of is that we have a steady income stream to make the most of what we really want to do – now and in retirement. That’s where the power of financial advice has been proven to help those with a goal achieve what they want.

Of those who set goals with a financial adviser, 86% said financial advice helped them achieve their goals.*

This key insight came to light in a groundbreaking survey of over 12,000 Australians in conjunction with CoreData. It found the benefits of financial advice helped no matter your age, wealth or gender. So, if you want to achieve your very own goal and have a comfortable life, it’s more likely to happen with some financial advice.

LT can provide you with professional advice for your financial planning needs. Call us today to arrange a meeting.

Source

*IOOF Survey 2020: The True Value of Advice – A study of 12,643 Australians is an Authorised Representative of Lonsdale Financial Group, ABN 76 006 637 225, AFSL No 246934. This is general advice only and does not take into account your objectives, financial situation and needs. Before acting on this advice, you should consult a financial adviser.

-

Asset Protection for Business Owners

Business owners will often reflect on Asset Protection as something they ‘should have done’ which can be painfully costly.

Asset protection is a necessity. It allows individuals to make a legal distinction between their personal and business assets. Courts don’t often respond well to assets being sold off after the initiation of a lawsuit, therefore this should be a proactively implemented strategy rather than a reactive one. If a strategy is not put into place, then this can lead to loss of whichever assets are available during a lawsuit; such as homes, cars, boats, etc.

Having strategies in place can prevent seizure of your assets, but can also act as a deterrent against potential claims. There are different types of asset protection plans. Consulting an advisor on which strategy is suitable for your business and industry will enable you to make a more informed decision as this can be a complicated process.

Speak with your LT accountant to discover more about protecting your assets.

-

Are you using cash flow forecasting in your business?

Cash flow problems are the reason that 82% of small businesses fail. One of the ways you can prevent your business from being one of them is by using a cash flow forecast.

Small business owners are often faced with stressful financial decisions and periods of uncertainty. Having a cash flow forecast can help your business avoid cash shortages by allowing you to track whether your spending is on target, prepare for business expansion, plan for upcoming cash gaps and plan budgets.

Here are some tips on cash flow forecasting to help your business be in control of its finances.

Prepare a sales forecast:

Existing businesses can look at past year’s sales figures, taking note of busy and quiet periods, and prepare an income prediction based on historical trends.

If you’re a new business, you can start by making cash outflow estimates. This can help you plan for what sales you should aim for to cover this and make estimates of predicted sales.

Knowing how much money you’ll have in a week or a month is central to being able to budget and know when to pay your expenses. Whether you receive customer payments at the time of sale, or you receive payments based on a subscription or service, you can schedule expenses and budget based on payment periods.

Account for other income forms:

Your business may generate income from sources other than customers. Having an estimate of what income you’ll receive and when allows you to refine your budget and plan around payments. These income sources could include:

• Grants (such as government grants).

• Tax refunds and GST rebates.

• Investments in the business.

• Deposits.

• Loans.Estimate your expenses:

Your cash flow forecast should include all your predicted expenses, giving you a detailed outline of the amount you’ll spend and when to help you determine a budgeting schedule and avoid cash shortages.

Expenses to consider in your forecast include:

• Bills such as electricity, water, rent, telephone and internet.

• Staff wages, including taxes, superannuation or bonuses.

• The cost of supplies and equipment.

• Packaging and delivery services.

• Software subscriptions, such as an office messaging system, accounting system, antivirus protection, website developing etc.