CASH FLOW BOOST PAYMENTS INFORMATION

Legislation has been released to support the government’s Cash Flow Boost Payments for SMEs which was part of the second stimulus package – the Boosting Cash Flow for Employers (Coronavirus Economic Response Package) Act 2020 (the Act).

Further to our last update, we can now clarify how your business may benefit from the cash flow boost payments, or PAYG withholding relief as we have previously referred to them.

Monthly PAYG withholding remitters

Overview

You will receive the following:

- one round of payments, based on your actual PAYG withholding from salaries and wages, payable following lodgement of each BAS and IAS from March to June 2020; PLUS

- a second round of payments, equal to the total of what you received in the first round, payable in four equal amounts following lodgement of each BAS and IAS from June to September 2020.

We stress again that the “payment” will come in the form of a credit to your RBA with the ATO. To the extent the credit puts you in a refund position for that particular BAS or IAS, you will be refunded within 14 days.

In more detail

If you lodge your BAS monthly you will receive the following credits to your BASs for the months of March through to September 2020:

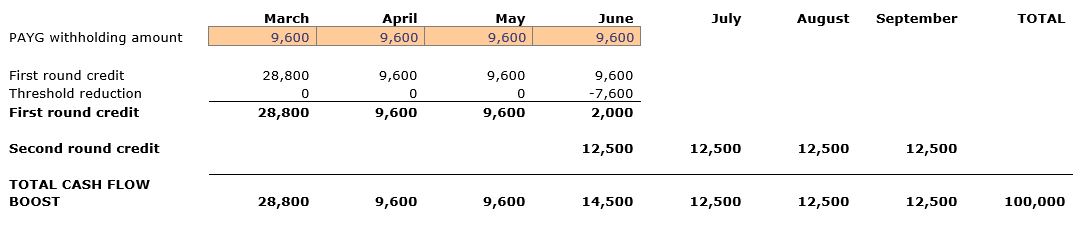

March – a first round credit equal to three times your reported/actual PAYG withholding amount from salaries and wages for March, with a minimum credit of $10,000 (even if you have no reported/actual PAYG withholding liability for March), and a maximum credit of $50,000.

April – a first round credit equal to your reported/actual PAYG withholding amount from salaries and wages for April. The credit for April will be reduced to the extent that your credits for March and April total more than $50,000.

May – a first round credit equal to your reported/actual PAYG withholding amount from salaries and wages for May. The credit for May will be reduced to the extent that your credits for March, April and May total more than $50,000.

June – a first round credit equal to your reported/actual PAYG withholding amount from salaries and wages for June. The credit for June will be reduced to the extent that your credits for March, April, May and June total more than $50,000. PLUS a second round credit equal to 25% of your total first round credits.

July – a second round credit equal to 25% of your total first round credits.

August – a second round credit equal to 25% of your total first round credits.

September – a second round credit equal to 25% of your total first round credits.

Example

You operate an eligible small business and have a reported/actual liability for PAYG withholding from salaries and wages of $9,600 for March 2020. Assume your PAYG withholding liability is consistently $9,600 for the months to June 2020.

Quarterly PAYG withholding remitters

Overview

Quarterly remitters will receive the following:

- one round of payments, based on the actual PAYG withholding from salaries and wages, payable following lodgement of the March BAS/IAS and the June BAS/IAS; PLUS

- a second round of payments, equal to the total of what was received in the first round, payable in two equal amounts following lodgement of the June BAS/IAS and the September BAS/IAS.

The payment will come in the form of a credit to the RBA and paid to the extent this creates a refund position for that particular BAS/IAS. The first payment therefore won’t happen until around the end of April 2020.

In more detail

March – a first round credit equal to the reported/actual PAYG withholding amount from salaries and wages for the March quarter, with a minimum credit of $10,000 (even if no amount is actually withheld for the March quarter), and a maximum credit of $50,000.

June – a first round credit equal to the reported/actual PAYG withholding amount from salaries and wages for the June quarter. The credit for June will be reduced to the extent that the credits for the March and June quarters total more than $50,000. PLUS a second round credit equal to 50% of the total first round credits.

September – a second round credit equal to 50% of the total first round credits.

Example

You operate an eligible small business and have a reported/actual liability for PAYG withholding from salaries and wages of $10,000 for the March 2020 quarter, and $15,000 for the June 2020 quarter.

For more help with regards to this and other stimulus package measures please speak with one of our accountants.