This article illustrates the importance of budgeting, saving and structuring loans to work in your favour, rather than purchasing on credit. The examples reiterate the importance of professional advice in early adult life to establish good habits and build financial knowledge. A great article for teens and young adults to demonstrate how much interest you may pay over your lifetime.

——————————————————

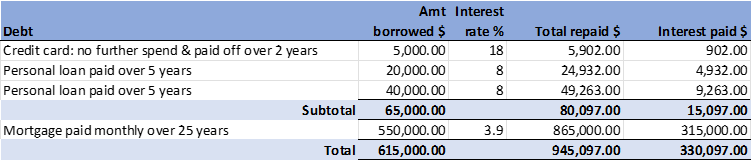

At 20 years old Jaxon graduated TAFE and found an administration job with a transport company.

He immediately applied for a credit card, embracing the convenience of online shopping, streaming subscriptions and tap-and-go facilities, and finally, he could join his friends at concerts, ski weekends and Bali holidays.

His credit card soon maxed-out at its $5,000 limit. Jaxon was shocked at how quickly his spending had added up. He reluctantly disciplined himself and committed to paying it off. It took two years!

While repaying his credit card, he couldn’t save, so when Jaxon bought a car, he borrowed the entire $20,000.

Jaxon’s loans and credit card meant that his pay was spent before he received it. He began to see interest on borrowings as a fact of life, never considering how much it was costing him.

Five years later, having repaid his debts, Jaxon upgraded to a brand new car with all the latest gadgets, this time borrowing $40,000.

This chart shows the amount of interest Jaxon had paid before he turned 30.

In ten years, Jaxon had paid over $15,000 in interest. When eventually he bought his first home, his interest payments really blew out.

Presumably, Jaxon will buy several cars and another home or two over his lifetime; he could easily end up paying more than a million dollars in interest.

When buying assets, and creating a lifestyle, interest often can’t be avoided, but it is possible to reduce the amount you pay.

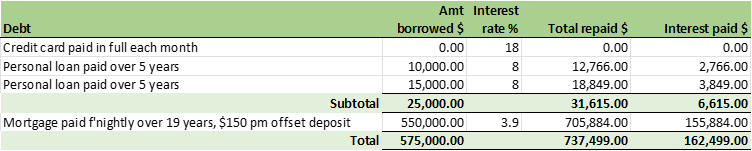

At 20, when Angela took out a credit card, she insisted on the lowest credit limit possible and ensured she paid the full card balance each month. The low credit limit meant she’d have money for emergency purchases but never more than she could easily repay in a couple of months.

Her parents introduced her to their financial adviser, who helped Angela create a budget and open a regular savings plan. Angela asked her employer to direct a set amount into it each pay. She didn’t miss the money, and her budget helped her stay on track with card payments and discretionary spending.

After a year of saving, Angela bought her first car. With her savings, she only needed to borrow half the car’s value. As her repayments were easily managed, she continued saving.

Again using her savings, Angela eventually upgraded to a new car borrowing only half the value.

The chart below shows that over ten years, Angela paid significantly less interest than Jaxon but had made the same purchases.

When Angela was ready to purchase a house, she opted to make fortnightly repayments instead of monthly, and the money she’d previously deposited into her savings plan now went into a mortgage offset account.

Mortgage offsets are a great way to reduce the loan period and the interest paid over the course of the loan.

Consequently, Angela ended up paying considerably less interest than Jaxon. This was no accident.

Early on, Angela had sought professional advice, she’d budgeted and saved, and structured her loans to work in her favour. Instead of relying on her credit card, Angela lived frugally, saved and paid cash wherever possible.

Additionally, Angela and her financial adviser regularly reviewed her financial position to ensure her savings and borrowing arrangements continued to meet her needs.

Few of us purchase big-ticket items without borrowing. Interest is the price we pay for those things that facilitate our chosen lifestyle. But while interest may be a necessary evil, we really can take control of our finances and ensure we don’t pay more than we have to.

Disclaimer :

The information contained in this article is for general information purposes only, professional advice should be obtained before acting on any information contained herein. Neither the publishers nor the distributors can accept any responsibility for loss occasioned to any person as a result of action taken or refrained from in consequence of the contents of this publication.