Ah, Christmas! It’s that magical time of year when Santa Claus jets across the world delivering presents, joy, and sugar-induced meltdowns for parents everywhere. But as seasoned accountants and financial planners know, even Santa’s North Pole operation can’t run on Christmas cheer alone. Behind the festive façade of elves, flying reindeer, and “free” gifts lies a complex financial engine that would make even the sharpest CFO sit up and take notice.

So, let’s take a light-hearted peek into how Santa might manage his books and finances—and how he could use a little real-world accounting advice from Leenane Templeton.

1. Santa’s Revenue Streams: A Questionable Income Statement?

Santa may be magical, but his revenue model is about as clear as a Queensland storm in December. On paper, he gives away millions of gifts every year with no obvious cash flow. If you’ve ever wondered whether Santa’s operation is eligible for not-for-profit status, you’re not alone.

Hypothetically, we might classify Santa’s “clients” (children worldwide) as beneficiaries of his goodwill services. But even the ATO would raise an eyebrow if billions of dollars’ worth of toys, games, and gadgets appeared on the North Pole’s ledger with no sales income.

Santa Tip: Maybe it’s time to consider monetising his brand. Merchandise? Movie deals? “Elf-on-the-Shelf” royalties? Santa, mate, you’re sitting on an intellectual property goldmine.

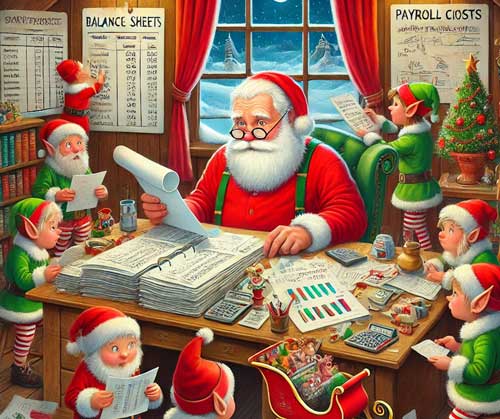

2. North Pole Payroll: Managing Elf Employment Costs

The elves are Santa’s most valuable resource—and probably his largest expense. With year-round toy production and a strict Christmas Eve deadline, the elves clearly operate under a high-pressure environment. Imagine the overtime costs!

On the bright side, Santa could claim some labour cost deductions… assuming elves are classified as employees and not independent contractors (the ATO loves those distinctions). Of course, we’ll need to factor in superannuation. What’s 11% of an elf’s annual wage? Or do they get paid in gingerbread?

HR Consideration: Santa may want to review his Fair Work compliance. If the elves unionise, he could have a Christmas catastrophe on his hands.

3. Depreciating the Sleigh: Capital Works Deductions

A sleigh capable of circumnavigating the globe in 24 hours doesn’t come cheap. Throw in eight (or nine, if you include Rudolph) flying reindeer, and Santa’s got some serious maintenance expenses. Fuel costs? Practically zero. But what about reindeer feed, veterinary bills, and sleigh repairs?

Our recommendation: Santa needs to capitalise on depreciation schedules. A sleigh of this calibre surely qualifies for capital works deductions under Division 40. If he depreciates the asset over 30 years, he’ll save a fortune on his taxes—provided he lodges a return.

Side Note: Santa, if you’re reading this, please don’t forget to keep receipts. It’s a lot harder to claim repairs on magical assets without the paperwork.

4. Santa’s Inventory Management: Toy Manufacturing Woes

Santa’s toy production facility is a marvel, but inventory management is key. Stocking millions of toys, categorising them by naughty and nice children, and storing everything pre-Christmas sounds like a logistical nightmare.

If Santa isn’t already using advanced ERP software, we’d strongly advise it. Even a mythical operation needs proper inventory controls to avoid costly overstocking of outdated fidget spinners in 2024.

Pro Tip: Write off obsolete toys before the ATO knocks on the door of the North Pole.

5. Global Tax Obligations: Naughty List or Tax Audit?

Santa may be based in the North Pole, but his global gift delivery model exposes him to tax laws across countless jurisdictions. Think of the complexity—import duties, customs fees, fringe benefits tax (FBT) on gifts, and GST! Does Santa include a receipt in every present to meet invoicing requirements?

Given Santa’s “gift-giving” business model, the ATO could argue that his presents are a form of non-monetary compensation, and therefore taxable. Can you imagine the fine print? “Congratulations, Timmy! Here’s your LEGO set… and a $50 tax liability to boot.”

6. Retirement Planning: Super for Santa?

Let’s face it: Santa’s been working for centuries. At this stage, he should have a solid self-managed super fund (SMSF) in place and a diversified investment portfolio. How else does he fund the North Pole’s operations during off-season months?

We’d suggest Santa consider a retirement plan that reduces his workload. Maybe hand over the reins to Mrs Claus, start a part-time gig at Myer photoshoots, or transition to “consulting” roles. After all, even legends deserve a break.

7. What about you? What happens when you leave out carrots for the reindeer and mince pies for Santa? How do you account for it?

Is it a gift, an entertainment expense, or perhaps an elaborate bribe to ensure you stay on the “nice” list? The ATO might argue it falls under “entertainment,” given that Santa enjoys his pie mid-delivery, but good luck claiming a deduction for a non-corporeal guest.

Meanwhile, the carrots for the reindeer could technically count as “livestock feed,” though explaining that in an audit may leave you redder than Rudolph’s nose. Best to just chalk it up as a festive goodwill expense—and hope Santa doesn’t issue a GST invoice for his services!

Wrapping It Up (With a Bow)

Running a global, centuries-old operation like Santa’s is no easy feat. From managing elves to appeasing the ATO, it’s clear even the jolly man in red could benefit from sound financial planning and accounting advice.

So, if you’re reading this, Santa, give us a call before 30 June 2025. We’ll make sure your books are balanced, your sleigh is depreciated, and your elves are happy. After all, no one wants to see Christmas cancelled over a tax audit.

From all of us at Leenane Templeton we wish you a merry Christmas and a financially sound New Year! 🎄

Disclaimer: This article is a humorous take on Santa’s “business” and not intended as financial advice. Please contact us for actual accounting and tax planning services—Santa included.