You may pay less tax with the tax cuts that have taken effect from 1 July. While the tax savings will depend on your circumstances, it’s important to think about the best way to use them.

For some of us, the savings may be needed to meet regular household expenses and manage cost of living increases. But if you have capacity, there are ways you may be able to use the tax savings to improve your financial position, such as reducing debt, investing or boosting your super.

The key is to make a conscious decision to put the tax savings to work in a way that suits you.

Who benefits from the changes?

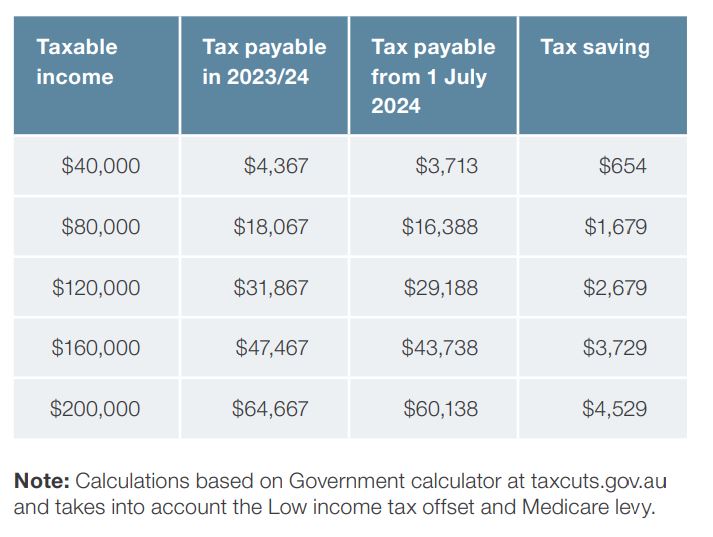

The Government estimates approximately 13.6 million Australian taxpayers will pay less tax when the ‘Stage 3 tax cuts’ commenced from 1 July. The table on this page illustrates the potential tax savings at different taxable incomes. To estimate your tax savings, check out the calculator in the taxcuts.gov.au website.

Smart ways to use your tax savings

There are many options to consider if you’d like to put your tax savings to work.

You may want to make additional mortgage repayments, where you can effectively ‘earn’ the loan interest rate tax-free.

Another option is investing in your own name, such as in term deposits, shares or managed investments. This could suit when planning for certain goals where you may need to access the money before you retire, like children’s education. You could also consider contributing to super, where there may be significant tax and other benefits. For instance:

• you may be able to arrange for your employer to contribute some of your pre-tax salary into super, via ‘salary sacrifice’ (see the case study)

• you may be able to claim personal super contributions as a tax deduction

• if you’re a lower income earner and make personal contributions, you may be eligible for a Government co-contribution of up to $500, and

• if you contribute on behalf of a low-income spouse, you may be eligible for a tax offset of up to $540.

But remember, there are caps on how much you can contribute to super and additional tax and penalties may apply if you exceed the caps. Also, you can’t access the money until you retire or meet other conditions.

Case Study

Using your tax cut to boost your super with salary sacrifice

Horace, aged 55, earns a taxable income of $120,000 and his tax savings in 2024/25 will be $2,679. He wants to boost his retirement savings using super.

His financial adviser works out that even though his tax savings will be $2,679 after tax, he could salary sacrifice as much as $3,940 before tax and still receive the same after-tax income in 2024/25. This is because salary sacrifice contributions are made with pre-tax dollars.

His super fund will deduct 15% tax from the amount he salary sacrifices, which will reduce the contribution to $3,349. But this is still $670 more than the tax saving of $2,679 he would have received as additional take-home pay if he didn’t salary sacrifice.

How you can benefit?

We can help you work out how you could beneficially use your tax cut from 1 July to achieve your short, medium and longer term goals.